Saving tax is not just about reducing your liability—it is about smart financial planning. Every year, many taxpayers in India miss out on deductions simply because they are unaware or do not plan in advance. With the start of Financial Year 2026–27, this is the perfect time to prepare a proper tax-saving checklist.

In this article, we will cover everything you need in simple language, including deductions under Section 80C, 80D, 80E, 80G, benefits of HRA and LTA, National Pension System (NPS), and also the limitations of the new tax regime.

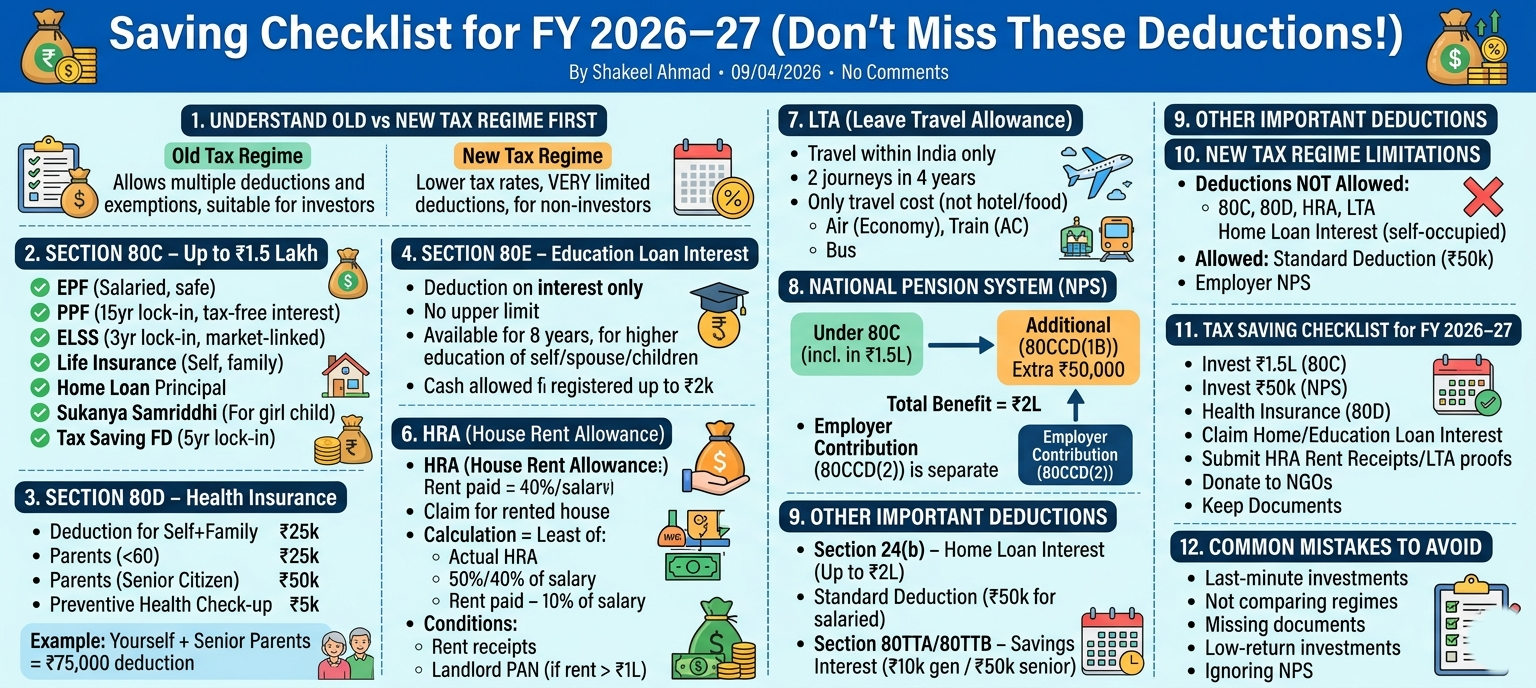

1. Understand Old vs New Tax Regime First

Before planning your tax savings, the first step is to choose the right tax regime.

Old Tax Regime

- Allows multiple deductions and exemptions

- Suitable if you invest and claim deductions

New Tax Regime

- Lower tax rates

- Very limited deductions allowed

👉 Important: If you don’t invest or claim deductions, new regime may be better. But if you actively save tax, old regime usually gives more benefit.

2. Section 80C – Most Important Deduction (Up to ₹1.5 Lakh)

This is the most popular and widely used tax-saving section.

Maximum Deduction

- ₹1,50,000 per year

Popular Investment Options:

1. Employee Provident Fund (EPF)

- Automatically deducted for salaried employees

- Safe and guaranteed returns

2. Public Provident Fund (PPF)

- Lock-in: 15 years

- Tax-free interest

- Good for long-term savings

3. Equity Linked Savings Scheme (ELSS)

- Lock-in: 3 years (shortest)

- Market-linked returns

- Suitable for higher returns

4. Life Insurance Premium

- Premium paid for self, spouse, children

- Policy must be active

5. Principal Repayment of Home Loan

- EMI principal portion is eligible

6. Sukanya Samriddhi Yojana

- For girl child

- High interest rate + tax benefit

7. Tax Saving Fixed Deposit

- Lock-in: 5 years

- Safe but lower returns

👉 Tip: Try to start investing early in the year instead of rushing in March.

3. Section 80D – Health Insurance Deduction

Health insurance not only protects your health but also saves tax.

Deduction Limits

| Category | Deduction Limit |

|---|---|

| Self + Family | ₹25,000 |

| Parents (<60 years) | ₹25,000 |

| Parents (Senior Citizen) | ₹50,000 |

Preventive Health Check-up

- Up to ₹5,000 included in above limits

👉 Example:

If you pay insurance for yourself and senior citizen parents:

- Total deduction = ₹25,000 + ₹50,000 = ₹75,000

4. Section 80E – Education Loan Interest

If you have taken a loan for higher education, this section is very useful.

Key Points

- Deduction on interest only (not principal)

- No upper limit

- Available for 8 years

Eligible Loans

- For self, spouse, or children

- Must be from bank or financial institution

👉 Tip: Keep interest certificate from bank every year.

5. Section 80G – Donations

Donations to eligible institutions can help you save tax.

Deduction Types

- 100% deduction (with or without limit)

- 50% deduction

Important Points

- Donation must be to registered institutions

- Cash donation allowed only up to ₹2,000

- Above that, use online or cheque

👉 Example:

Donation of ₹10,000 may give deduction of ₹5,000 or full ₹10,000 depending on eligibility.

6. HRA (House Rent Allowance)

If you are living in a rented house, HRA can significantly reduce tax.

HRA Calculation (Least of 3)

- Actual HRA received

- 50% of salary (metro) or 40% (non-metro)

- Rent paid – 10% of salary

Conditions

- Must be paying rent

- Rent receipts required

- PAN of landlord needed if rent > ₹1 lakh/year

👉 Tip: Even if you live with parents, you can pay rent and claim HRA (with proper documentation).

7. LTA (Leave Travel Allowance)

LTA helps you save tax on travel expenses.

Key Features

- Covers travel within India only

- Available for 2 journeys in 4 years

- Only travel cost (not hotel or food)

Allowed Travel Modes

- Air (economy class)

- Train (AC class)

- Bus (public transport)

👉 Tip: Keep tickets and boarding passes safely.

8. NPS (National Pension System) – Extra Tax Benefit

NPS is one of the best tools for retirement + tax saving.

Deduction Structure

Under 80C

- Included in ₹1.5 lakh limit

Additional Deduction (80CCD(1B))

- Extra ₹50,000

👉 Total Benefit = ₹2,00,000

Employer Contribution (80CCD(2))

- Additional benefit (no upper cap in many cases)

- Not counted in ₹1.5 lakh limit

👉 Tip: NPS is best for long-term retirement planning with tax advantage.

9. Other Important Deductions

Section 24(b) – Home Loan Interest

- Up to ₹2 lakh deduction for self-occupied property

Standard Deduction

- ₹50,000 for salaried employees and pensioners

Section 80TTA / 80TTB

- Savings account interest deduction

- ₹10,000 (general)

- ₹50,000 (senior citizens)

10. New Tax Regime – Limitations You Must Know

The new tax regime looks simple but comes with major limitations.

Deductions NOT Allowed

- ❌ Section 80C (PPF, LIC, ELSS etc.)

- ❌ Section 80D (health insurance)

- ❌ HRA

- ❌ LTA

- ❌ Home loan interest (for self-occupied property)

What is Allowed

- ✔ Standard deduction (₹50,000)

- ✔ Employer NPS contribution

👉 Conclusion:

If you want flexibility and tax-saving investments, old regime is better.

11. Tax Saving Checklist for FY 2026–27

Here is a simple checklist you can follow:

Investments

- ✔ Invest ₹1.5 lakh under 80C

- ✔ Invest ₹50,000 in NPS (extra benefit)

Insurance

- ✔ Buy/renew health insurance (80D)

- ✔ Check life insurance coverage

Loans

- ✔ Claim home loan interest

- ✔ Claim education loan interest (80E)

Salary Benefits

- ✔ Submit rent receipts (HRA)

- ✔ Claim LTA with proof

Donations

- ✔ Donate to eligible NGOs (80G)

Documents

- ✔ Keep all proofs safely

- ✔ Submit to employer on time

12. Common Mistakes to Avoid

Many taxpayers lose money due to simple mistakes:

1. Last-minute investments

- Leads to poor choices

2. Not comparing tax regimes

- May result in higher tax

3. Missing documents

- Claims can be rejected

4. Over-investing in low-return options

- Balance between tax saving and returns is important

5. Ignoring NPS

- Missing extra ₹50,000 benefit

13. Smart Tax Planning Tips

- Start tax planning in April, not March

- Diversify investments (PPF + ELSS + NPS)

- Use online tools for tax calculation

- Keep digital copies of all documents

- Review your tax plan every 6 months

Final Words

Tax saving is not about avoiding tax—it is about making smart financial decisions. If you plan properly, you can save a significant amount every year while also building wealth.

For FY 2026–27, make sure you:

- Use all major deductions like 80C, 80D, 80E, 80G

- Take advantage of HRA and LTA

- Invest in NPS for extra benefit

- Carefully choose between old and new tax regime

Start early, stay organized, and don’t miss any deductions!

Frequently Asked Questions (FAQs)

1. What is the maximum deduction allowed under Section 80C for FY 2026–27?

The maximum deduction allowed under Section 80C is ₹1.5 lakh per financial year. This includes investments like PPF, ELSS, LIC premium, EPF, and home loan principal repayment.

2. Can I claim both 80C and NPS deductions together?

Yes, you can claim both.

- ₹1.5 lakh under Section 80C

- Additional ₹50,000 under Section 80CCD(1B) for NPS

👉 Total benefit = ₹2 lakh

3. Is health insurance premium eligible for tax deduction?

Yes, under Section 80D:

- ₹25,000 for self and family

- ₹25,000/₹50,000 for parents (depending on age)

4. Can I claim HRA if I live with my parents?

Yes, you can claim HRA if you pay rent to your parents and maintain proper documentation like rent receipts and bank transfers. Your parents must show this rent as income in their tax return.

5. What deductions are not allowed in the new tax regime?

In the new tax regime, most deductions are not allowed, including:

- Section 80C

- Section 80D

- HRA

- LTA

- Home loan interest (self-occupied)

6. Is education loan interest fully tax deductible?

Yes, under Section 80E, the entire interest paid on an education loan is deductible with no upper limit, for up to 8 years.

7. Can I claim both HRA and home loan benefits together?

Yes, if you meet conditions (for example, living in a rented house in a different city while owning a house elsewhere), you can claim both HRA and home loan deductions.

8. Are donations eligible for 100% tax deduction?

Some donations qualify for 100% deduction under Section 80G, while others qualify for 50%. It depends on the institution and category of donation.

9. Is LTA applicable every year?

No, LTA can be claimed for 2 journeys in a block of 4 years. It only covers travel expenses within India.

10. Which tax regime is better for saving tax?

- Old regime is better if you claim multiple deductions (80C, 80D, HRA, etc.)

- New regime is better if you prefer simplicity and don’t invest much

👉 You should calculate tax under both regimes before deciding.