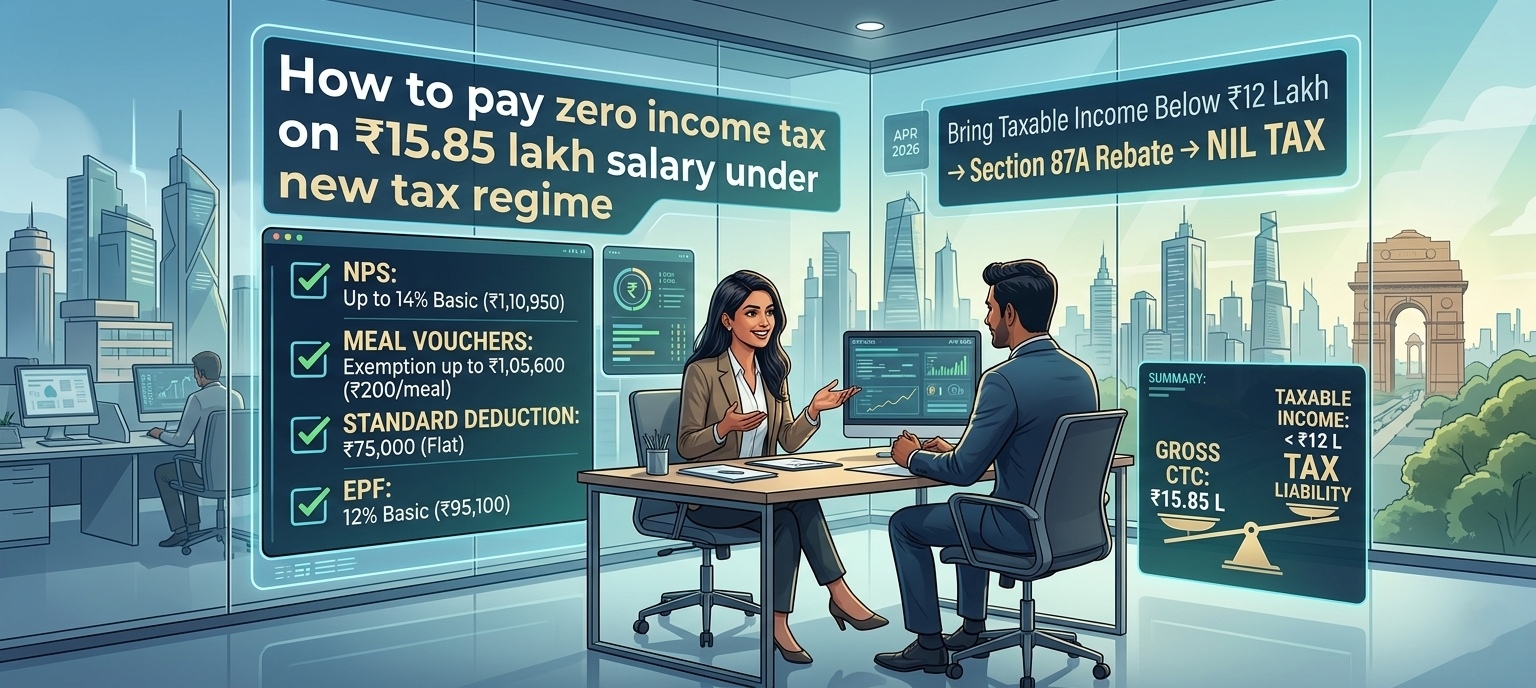

Pay Zero Income Tax on ₹15.85 Lakh Salary Under New Tax Regime (2026-27)

For the modern Indian professional, the journey from “Gross CTC” to “Net Take-Home” often feels like a gauntlet of deductions, levies, and surcharges. Historically, reaching a salary of ₹15 lakh and above meant graduating into the highest tax brackets, where a significant portion of your hard-earned money vanished into the government’s coffers.

However, the fiscal landscape of 2026 has brought a paradigm shift. With the recent refinements to the New Tax Regime and the expansion of the Section 87A rebate, there is a mathematically precise, 100% legal pathway to earning ₹15.85 lakh per annum while paying zero income tax.

This article explores the nuances of salary structuring, the psychology of tax-efficient compensation, and the specific legal provisions that make this “financial miracle” possible for Indian taxpayers.

I. The Philosophical Shift: Old Regime vs. New Regime

To understand how to pay zero tax on ₹15.85 lakh, we must first understand the philosophy of the New Tax Regime (Section 115BAC).

For decades, the Old Regime encouraged “forced savings” through Section 80C, 80D, and HRA. While beneficial, it required taxpayers to lock up liquidity in LIC policies, ELSS, or high-interest home loans just to save tax.

The New Tax Regime, specifically as of the Union Budget 2025 and 2026 updates, aims for a simpler structure with lower rates but fewer deductions. The “secret sauce” lies in the fact that while most deductions were removed, a few critical exemptions were retained and even enhanced. These remaining “carve-outs” are the levers we will use to bring a ₹15.85 lakh salary down to a taxable income of ₹12 lakh.

Why ₹12 Lakh is the “Golden Number”

The most pivotal update in recent tax history is the extension of the Section 87A Tax Rebate.

- Under the current rules, if your Net Taxable Income does not exceed ₹12,00,000, your tax liability is calculated, and then a rebate is applied to make the final payable amount zero.

- If you earn even ₹1 above this limit (subject to marginal relief rules), you could end up paying tax on the entire amount based on the slab rates.

- Therefore, our goal is to bridge the ₹3.85 lakh gap between your ₹15.85 lakh salary and the ₹12 lakh tax-free ceiling.

II. The First Pillar: The Universal Standard Deduction

The first step is the most straightforward. The government provides a Standard Deduction to all salaried individuals to account for the costs associated with employment (commuting, professional attire, etc.).

As of FY 2026-27, the Standard Deduction stands at ₹75,000.

- The Logic: This is a “flat” deduction. You do not need to submit fuel bills, bus tickets, or blazer receipts to your HR. It is applied automatically.

- The Calculation: > ₹15,85,000 (Gross) – ₹75,000 (Standard Deduction) = ₹15,10,000

III. The Second Pillar: Smart Salary Perquisites (Meal Vouchers)

This is where most taxpayers miss out. Many view “Salary” as a single block of cash, but a “CTC” (Cost to Company) is a collection of different components. One of the most tax-efficient components is the Meal Voucher perquisite.

Under the Income-tax Rules, 2026, the exemption for meals provided by an employer has been significantly adjusted to keep pace with inflation in urban India.

- The Rule: Meals provided through non-transferable paid vouchers (like Sodexo or Pluxee) are exempt up to a specific limit per meal.

- The 2026 Advantage: The exemption has been scaled to ₹200 per meal for two meals a day.

- Annual Impact: * ₹200 (per meal) × 2 (meals/day) = ₹400 per day.

- Assuming 22 working days a month: ₹400 × 22 = ₹8,800/month.

- Annual Exemption: ₹1,05,600.

By opting for meal vouchers instead of a taxable “Special Allowance,” you reduce your taxable income by over a lakh without changing your actual purchasing power—you’re simply using a card to buy groceries or lunch instead of your debit card.

- Current Balance: ₹15,10,000 – ₹1,05,600 = ₹14,04,400

IV. The Third Pillar: Employer’s NPS Contribution (Section 80CCD(2))

While the New Tax Regime famously removed the ₹1.5 lakh deduction for employee contributions to PF/NPS (Section 80C), it strategically kept the Employer’s contribution to NPS under Section 80CCD(2).

This is arguably the most powerful tool for high-income earners in India today.

- The Limit: The Central Government allows a deduction for the employer’s contribution to your NPS account up to 14% of your Salary (where Salary = Basic + Dearness Allowance).

- The Strategy: Most companies set “Basic Salary” at 50% of the total CTC to manage provident fund and gratuity obligations.

- On a ₹15.85 lakh CTC, let’s assume a Basic Salary of ₹7,92,500.

- 14% of ₹7,92,500 = ₹1,10,950.

- The Benefit: This money is not “lost.” It is invested in your name in the National Pension System, earning market-linked returns (usually 9-12% historically). It is part of your wealth, yet the tax department treats it as “invisible” income for the current year.

- Current Balance: ₹14,04,400 – ₹1,10,950 = ₹12,93,450

V. The Fourth Pillar: Employer’s PF Contribution

Similar to the NPS, the Employer’s contribution to the Employee Provident Fund (EPF) is exempt from tax, provided the total contribution to PF, NPS, and Superannuation does not exceed ₹7.5 lakh in a year.

- The Math: In India, the statutory employer contribution is 12% of the Basic Salary.

- 12% of ₹7,92,500 (Basic) = ₹95,100.

- The Result: This amount is deducted from your Gross CTC to arrive at your taxable income. Like the NPS, this is “your money” sitting in a safe, government-backed retirement account earning tax-free interest (currently around 8.15%–8.25%).

- Final Taxable Income: ₹12,93,450 – ₹95,100 = ₹1,198,350

VI. The Final Verdict: Why You Pay Zero Tax

Now, let’s look at the final number. Your Net Taxable Income is ₹11,98,350.

Under the New Tax Regime for FY 2026-27:

Income up to ₹4,00,000: Nil

₹4,00,001 to ₹8,00,000 (10%): ₹40,000

₹8,00,001 to ₹12,00,000 (15%): ₹60,000

Total Calculated Tax: ₹1,00,000 (approximate, based on updated 2026 slabs)

HOWEVER, because your total income is below ₹12,00,000, Section 87A kicks in. The government provides a full tax rebate equal to your tax liability for anyone in this bracket.

Total Tax Payable: ₹0.

VII. Deep Dive: The Mechanics of Salary Structuring

Many employees mistakenly believe that they have no control over their salary structure. They sign an offer letter and accept the “Take-home” as a fixed reality. In the modern corporate world, this is a misconception.

Flexible Benefit Plans (FBP)

Most mid-to-large-tier companies in India (IT, Pharma, Banking, FMCG) now offer a Flexible Benefit Plan. This allows you to choose how your CTC is distributed. To achieve the zero-tax goal, you must actively select:

- NPS Corporate Model: Opt-in for the 14% employer contribution.

- Meal Cards: Opt for the maximum limit (₹4,400 to ₹8,800 monthly depending on company policy).

- Gift Vouchers: Many companies offer up to ₹5,000 per year in tax-free gift vouchers.

- Internet/Telephone Reimbursement: While not used in our ₹15.85L calculation, if your income is even higher, you can use these (usually ₹1,000–₹2,000/month) to further reduce taxable income.

The Role of HR

To implement this, you must communicate with your payroll department before the “Investment Declaration” window closes (usually in April or May). You cannot “claim” employer NPS or Meal Vouchers at the end of the year if they weren’t part of your monthly payroll process.

VIII. The "Marginal Relief" Safety Net

A common fear among taxpayers is: “What if I get a small bonus or a ₹10,000 raise? Will I suddenly have to pay ₹1 lakh in tax because I crossed the ₹12 lakh limit?”

Fortunately, the Income Tax Act provides Marginal Relief. If your income exceeds ₹12 lakh by a small margin, the tax you pay is capped at the amount by which your income exceeds ₹12 lakh.

Example: If your taxable income is ₹12,05,000, your tax won’t be ₹1,00,000+. It will be limited to the “extra” ₹5,000 you earned. This safety net ensures that earning more money never results in less money in your pocket after tax.

IX. Wealth Creation: The Hidden Benefit

This strategy isn’t just about “beating the system.” It is fundamentally about wealth optimization.

By structuring your salary this way, you are diverting:

- ₹1,10,950 into NPS (Equities/Bonds)

- ₹95,100 into EPF (Safe, Fixed Income)

- Total Annual Savings: ₹2,06,050

In 10 years, assuming a conservative 10% average growth, this “tax saving” alone will blossom into a corpus of over ₹35 Lakhs. By paying zero tax, you aren’t just saving money today; you are building a multi-million rupee retirement nest egg.

X. Potential Pitfalls and Disclaimers

While this roadmap is legally sound, there are variables to consider:

Other Income: If you have rental income from a flat, interest from Fixed Deposits, or capital gains from selling stocks, this income is added to your ₹11.98 lakh salary. If the total crosses ₹12 lakh, the zero-tax status vanishes.

Basic Salary Ratio: If your company fixes Basic Salary at 30% or 40% of CTC (instead of 50%), your NPS and EPF contribution limits will be lower, meaning you might have a small tax liability.

Professional Tax: This varies by state (usually ₹2,500/year). While it reduces taxable income, it’s a minor factor.

Tax Law Changes: This guide is based on the 2026 fiscal environment. Always check the latest circulars from the CBDT (Central Board of Direct Taxes).

XI. Conclusion: The Power of Information

The difference between a person who pays ₹1.2 lakh in tax and a person who pays ₹0 on a ₹15.85 lakh salary is not their income—it is their information.

The Indian government has designed the New Tax Regime to reward those who simplify their taxes and invest in long-term retirement vehicles like the NPS. By utilizing the Standard Deduction, maximizing the new meal voucher limits, and leveraging employer-based retirement contributions, the modern Indian professional can achieve the ultimate financial goal: Keeping 100% of their taxable income.

Take this guide to your HR department, review your “Salary Annexure,” and start your journey toward a tax-free 2026.

Summary Checklist for Your HR:

[ ] Is my Standard Deduction applied?

[ ] Can I opt for Meal Vouchers up to ₹8,800/month?

[ ] Is my Employer NPS Contribution set to 14% of Basic?

[ ] Is my EPF being contributed to by the employer at 12%?

[ ] Does my total Net Taxable Income fall below ₹12,00,000?

Frequently Asked Questions (FAQs)

1. Can I still claim the ₹12 lakh rebate if I have income from house property or bank interest?

The Section 87A rebate applies to your Total Taxable Income. If your salary is structured to bring you down to ₹11.98 lakh, but you earn an additional ₹10,000 in bank interest or rental income, your total income will hit ₹12,08,350. In this case, you would exceed the ₹12 lakh limit. However, thanks to Marginal Relief introduced in the 2025/26 updates, you wouldn’t pay the full tax on the entire amount; your tax would be capped at the extra ₹8,350 you earned above the threshold.

2. My HR says they don’t offer the “NPS Corporate Model.” Can I still get the 14% deduction?

No. To benefit from Section 80CCD(2), the contribution must be made by the employer on your behalf. If you contribute to NPS yourself, it is considered an “Employee Contribution.” Under the New Tax Regime, employee contributions (like those under 80C or 80CCD(1)) are not deductible. If your company doesn’t offer this, you might need to discuss a salary restructuring with your payroll department to include the corporate NPS component.

3. Why are meal vouchers so important in this calculation?

In the 2026 tax landscape, meal vouchers are one of the few “perquisites” that remain exempt under the New Tax Regime. Because the exemption limit was increased to ₹200 per meal, it allows you to shield over ₹1 lakh of your annual income from tax. Unlike a “Special Allowance,” which is fully taxable, meal vouchers are non-cash benefits that reduce your taxable “Gross Salary” at the source.

4. Is the ₹75,000 Standard Deduction only for the New Regime?

As of the latest fiscal updates, the Standard Deduction of ₹75,000 is available under both regimes. However, it is more “powerful” in the New Tax Regime because it acts as one of the primary tools to bring your income below the ₹12 lakh rebate ceiling. In the Old Regime, you would likely need many more deductions (HRA, 80C, 80D) to achieve a similar zero-tax result on a ₹15.85 lakh salary.