I. What is same in Income Tax Act 1961 and 2025?

- The basic purpose remains: to provide for levy, administration, collection and recovery of income tax in India. The Income Tax Act 2025 continues to “consolidate and amend the law relating to income-tax”.

- The tax slabs / rates for many taxpayer categories are retained under the new Tax Act (i.e., the government is not radically changing the rate structure as part of this overhaul) at least for now.

- Many of the underlying concepts (income heads, business profits, capital gains, etc.) carry over though with updated language.

II. What are major reforms in the Income Tax Act 2025?

1. Terminology: “Tax Year” instead of “Previous Year” or “Assessment Year

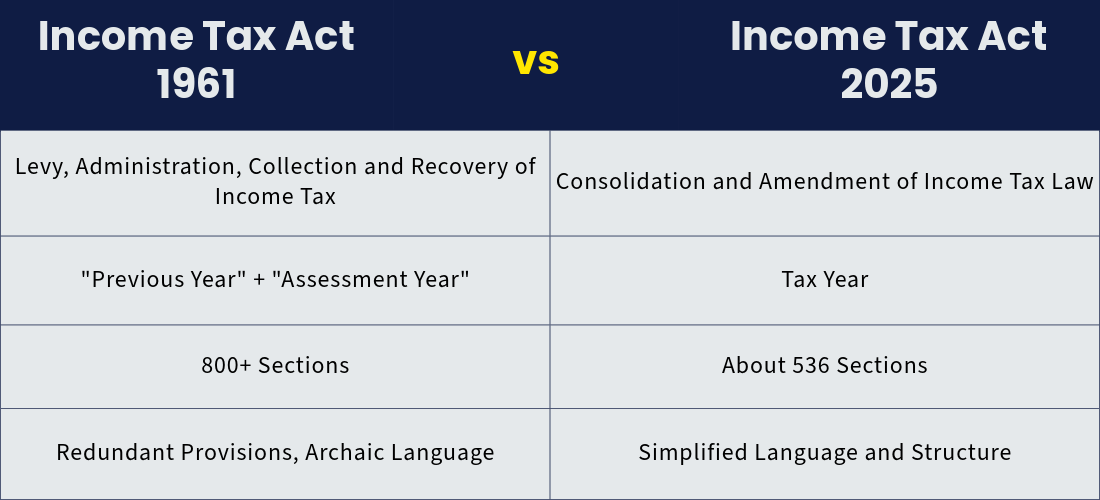

The Income Tax Act 1961 used two linked concepts: the “previous year” (the year in which income is earned) and the “assessment year” (the year in which that income is assessed). The 2025 Act introduces a single “tax year” concept (a 12-month period beginning 1 April) to simplify this.

2. Section in Income Tax Act 1961 vs 2025

Under the Income Tax Act 1961, the number of sections had grown (800+ after many amendments). The Income Tax Act 2025 reduces the section count (to about 536) and reorganises chapters and schedules.

3. Simplification of language and structure

The 2025 Act aims to remove redundant provisions, archaic language, confusing provisos/explanations, and to present the law in a more readable, systematic manner.

4. Digital-first / modern compliance architecture

The Income Tax Act 2025 emphasises faceless assessment, e-notices, digital workflows, reducing manual/human interface (in part).

5. Repeal of the 1961 Act & transition rules

The 2025 Act formally replaces the 1961 Act. However, for tax years beginning before the effective date of the 2025 Act the old Act continues to apply.

III. What are the key practical differences we should know?

- The Income Tax Act 2025 is scheduled to come into force from 1 April 2026 (unless otherwise specified).

- Because of the change in year-terminology, what was earlier called “previous year / assessment year” will be replaced by “tax year” in most contexts. This is meant to reduce confusion.

- The reduction in number of sections (from “700+” under 1961 Act to “536” under 2025) and the restructuring means practitioners will need to map old section numbers to new ones.

- While tax rates aren’t changing dramatically immediately, the overhaul may impact deductions, compliance burdens, definitions, and administrative process (which may affect tax planning).

- The older Act’s many amendments over decades had built in complexity; the new Act is trying to sweep away or simplify many legacy provisos, explanations and redundancies.

IV. What are the precautions we should take into consideration?

- Even though the new Act is in place, for income/tax years starting before 1 April 2026, the 1961 Act will continue to apply for many things.

- Some changes may be procedural (how you file, how assessments are done) rather than just substantive (rates, deductions). So it’s not just a “rename and re-number” exercise but a compliance change for tax professionals.

- Mapping: If you’ve used a lot of planning based on old section numbers (e.g., section 80C, 10 etc), you’ll need to check how the new Act re-labels or reorganises those provisions.

- Because the 2025 Act is a “fresh” law (not just a simple amendment), there may be some litigation or interpretation issues in the early years.

- Even though rate structure is retained for now, the government may use the new Act to introduce reforms in later years (so just because rates are same now doesn’t guarantee they stay the same).

V. Summary

-

The 1961 Act served India’s income-tax regime for over 60 years but had become bulky, complex and full of amendments.

-

The 2025 Act is a major overhaul — simplifying structure, language, processes, and aligning with modern compliance needs.

-

For tax payers and practitioners: many of your familiar things (rates, broad categories) remain, but the “packaging”, numbering, process and certain definitions/deductions may change.

-

The effective date is from April 2026, so there is some time to prepare and map old to new.