Choosing the right savings instrument is a cornerstone of financial planning in India. Among the most popular options are Fixed Deposits (FDs) and Recurring Deposits (RDs). Both are time-tested, low-risk, and offer guaranteed returns, making them favorites for conservative investors.

While they share many similarities, they cater to different financial habits and goals. This article explores the nuances of FD and RD to help you decide which fits your current financial situation.

1. Understanding the Basics

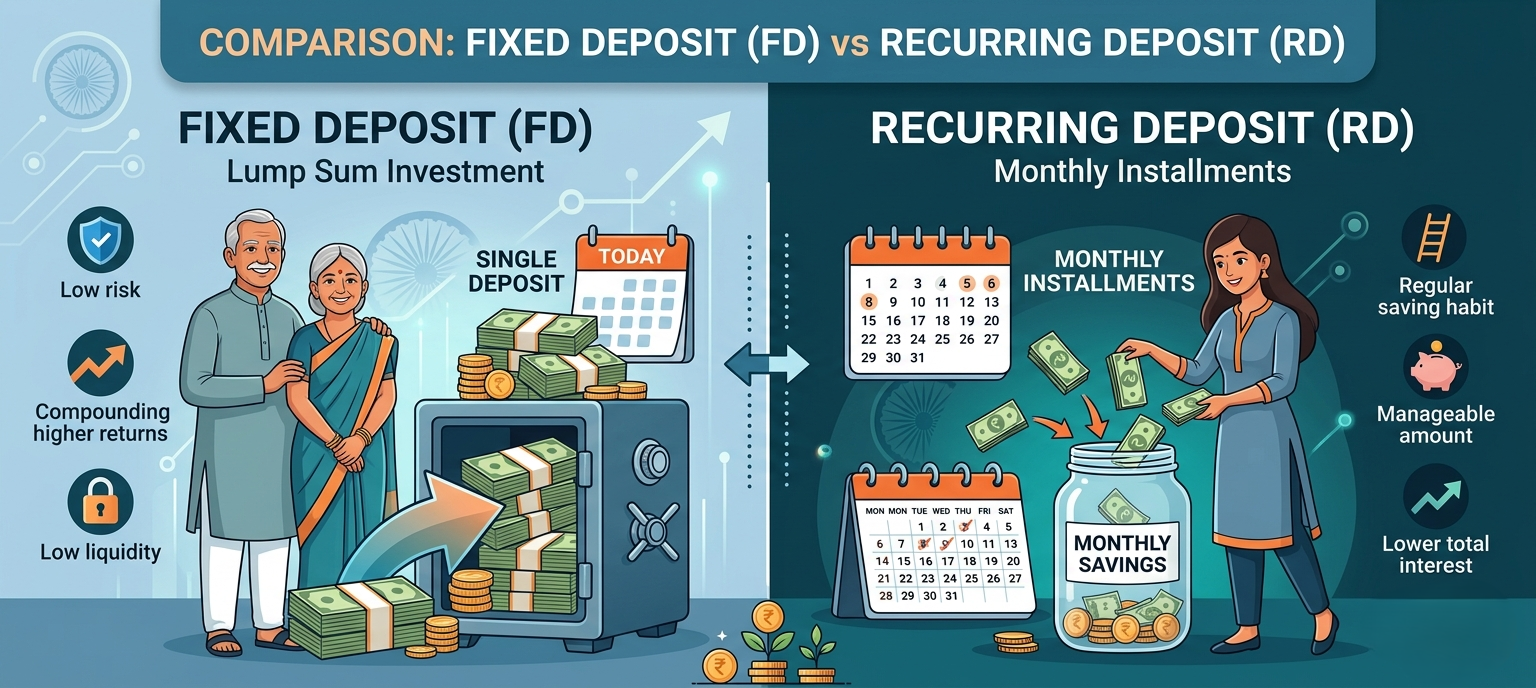

What is a Fixed Deposit (FD)?

A Fixed Deposit involves a one-time, lump-sum investment for a pre-determined period (tenure). Once you deposit the money, it stays with the bank until maturity, earning a fixed interest rate.

- Key Features: Lump-sum investment, fixed interest rate, tenure ranging from 7 days to 10 years.

- Benefits: Higher interest rates compared to savings accounts, high safety, and the ability to take a loan against the deposit.

- Drawbacks: Liquidity is limited (premature withdrawal often attracts a penalty), and the entire corpus must be available upfront.

What is a Recurring Deposit (RD)?

A Recurring Deposit is a disciplined savings tool where you deposit a fixed amount every month for a specific tenure. It is ideal for individuals with a regular monthly income who want to build a corpus over time.

- Key Features: Monthly installments, fixed interest rate, tenure usually between 6 months and 10 years.

- Benefits: Encourages regular saving, requires a small starting amount (as low as ₹100), and offers interest rates similar to FDs.

- Drawbacks: If you miss an installment, banks may levy a penalty. Like FDs, premature withdrawal reduces the effective interest earned.

2. Detailed Comparison Table

| Parameter | Fixed Deposit (FD) | Recurring Deposit (RD) |

| Investment Type | Lump sum (One-time) | Monthly installments |

| Tenure | 7 days to 10 years | 6 months to 10 years |

| Liquidity | Low (Premature withdrawal allowed with penalty) | Low (Premature withdrawal allowed with penalty) |

| Interest Rates | Generally slightly higher | Usually comparable to FDs |

| Risk | Very Low (RBI insured up to ₹5 Lakh) | Very Low (RBI insured up to ₹5 Lakh) |

| Tax Implications | Taxable at slab rates; TDS applicable | Taxable at slab rates; TDS applicable |

| Suitability | For those with idle surplus cash | For salaried professionals/regular earners |

| Ideal User Profile | Retirees, windfall gain recipients | Students, first-time earners, goal-based savers |

3. Interest Earnings Comparison

To understand the actual wealth creation, let’s compare a lump-sum FD versus a monthly RD over 5 years (60 months).

Assumptions (based on 2026-27 market rates):

- Interest Rate: 7.00% p.a. (compounded quarterly)

- Total Principal Invested: ₹6,00,000

Scenario 1: Lump Sum in FD

In this scenario, you invest ₹6,00,000 all at once at the start of Year 1.

- Principal: ₹6,00,000

- Tenure: 5 Years

- Maturity Value: ~₹8,48,866

- Interest Earned: ₹2,48,866

Logic: The entire amount earns 7% interest from Day 1, benefiting fully from compounding over the full 60 months.

Scenario 2: Monthly Installments in RD

In this scenario, you invest ₹10,000 every month for 60 months.

- Monthly Principal: ₹10,000 (Total ₹6,00,000)

- Tenure: 5 Years

- Maturity Value: ~₹7,17,000

- Interest Earned: ₹1,17,000

Logic: Only the first installment earns interest for 60 months. The last installment (deposited in the 60th month) only earns interest for 30 days.

The Verdict on Earnings: While the total principal is the same, the FD earns significantly more because the entire capital works for you from the very beginning.

4. Pros and Cons Summary

Fixed Deposit (FD)

Pros:

- Maximizes compounding benefits.

- Can be used as collateral for loans/credit cards.

- Tax-saving FDs (5-year lock-in) offer 80C benefits.

Cons:

- Requires a large initial capital.

- Funds are locked away; early exit costs money.

Recurring Deposit (RD)

Pros:

- Zero financial burden; manageable monthly outgo.

- Instills financial discipline.

- Protected from market volatility.

Cons:

- Lower total interest compared to an equivalent lump-sum FD.

- Penalty for missed installments.

5. Tax Implications (The "Fine Print")

In India, the taxation for both is identical but often misunderstood:

- Income Tax: The interest earned is added to your “Income from Other Sources” and taxed as per your individual Income Tax Slab.

- TDS (Tax Deducted at Source): Banks deduct 10% TDS if the total interest earned across all your deposits (FD + RD) in a bank exceeds ₹50,000 in a financial year (₹1,00,000 for Senior Citizens).

- Form 15G/15H: If your total annual income is below the basic exemption limit, you can submit these forms to prevent the bank from deducting TDS.

6. Conditional Verdict: Which should you choose?

Choose a Fixed Deposit (FD) if:

- You have received a bonus, inheritance, or gift and have no immediate use for it.

- You are a senior citizen seeking stable, maximum quarterly interest payouts.

- You want to claim a tax deduction under Section 80C (via 5-year Tax-Saver FDs).

Choose a Recurring Deposit (RD) if:

- You are a salaried professional with a fixed monthly surplus.

- You are saving for a specific short-term goal, like a vacation, an annual insurance premium, or a wedding.

- You do not have a large lump sum but want to start your investment journey today.

Conclusion

Both FDs and RDs are excellent safety nets for an Indian investor’s portfolio. The FD is the superior wealth builder for those who already have capital, while the RD is the superior habit builder for those looking to accumulate wealth slowly.

For a balanced approach, many investors use RDs to accumulate a small corpus over 12 months and then “roll it over” into a Fixed Deposit once it matures, effectively getting the best of both worlds. Whatever you choose, ensure it aligns with your liquidity needs and your tax bracket.

Frequently Asked Questions (FAQs)

1. Can I change the monthly installment amount or the date in an RD? No. Once you open a Recurring Deposit, the installment amount and the date of deduction are fixed for the entire tenure. If you wish to invest a different amount, you would typically need to open a second RD account.

2. Is the interest rate on FD and RD fixed for the whole duration? Yes. One of the biggest advantages of these deposits is that the interest rate is locked in at the time of opening. Even if market interest rates fall later, the bank must pay you the originally agreed-upon rate until your deposit matures.

3. What happens if I miss an RD installment? Most Indian banks allow a small grace period. However, if you miss the payment, a penalty (usually a few rupees per ₹100) is charged. If you miss several consecutive installments, the bank may prematurely close the RD and transfer the balance to your savings account after deducting applicable penalties.

4. Can I withdraw my money before the maturity date? Yes, both FDs and RDs allow premature withdrawal. However, banks usually charge a penalty of 0.5% to 1% on the interest rate. Additionally, you will receive interest only for the period the money actually stayed with the bank, not the original higher rate promised for the full tenure.

5. Is the interest earned on FDs and RDs tax-free? No. The interest earned is fully taxable. While the bank may deduct 10% TDS if your interest exceeds ₹50,000 in a year, this is not the final tax. If you are in the 30% tax bracket, you will have to pay the remaining 20% tax yourself when filing your Income Tax Return (ITR).