Complete Analysis, Key Announcements, Tax Changes & Impact on Personal Finance in India

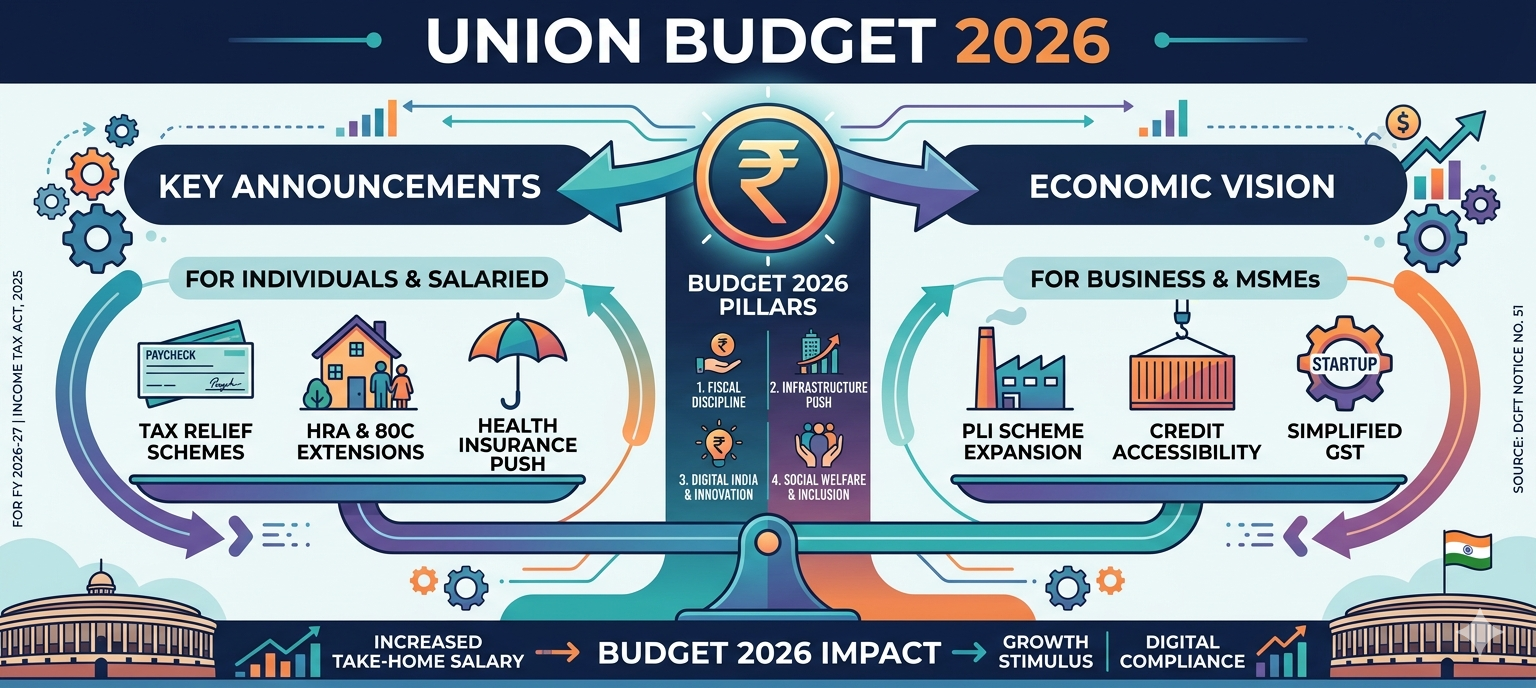

The Union Budget 2026 is one of the most anticipated economic events in India. Presented annually by the Government of India, the Union Budget outlines the government’s financial plan for the upcoming fiscal year. It provides insights into taxation policies, government spending, economic reforms, and development priorities.

Budget 2026 has focused on strengthening economic growth, boosting infrastructure investment, supporting startups and MSMEs, encouraging digital transformation, and improving the overall financial ecosystem of the country.

For individuals, investors, and businesses, understanding the key highlights of Budget 2026 and its impact on personal finance is essential. Changes in taxation rules, government spending priorities, and financial policies directly influence income planning, investment decisions, and business strategies.

In this article, we provide a detailed analysis of Budget 2026, including major announcements, tax reforms, sector-wise impact, and how individuals should plan their finances after the budget.

What is the Union Budget?

The Union Budget is the annual financial statement of the Government of India that presents the estimated revenue and expenditure for the upcoming financial year.

It is presented in Parliament by the Finance Minister of India, usually on 1st February every year.

The budget includes:

- Government income (tax and non-tax revenue)

- Government expenditure

- Fiscal deficit targets

- Policy reforms

- Sector-wise allocations

- Economic growth strategies

The Union Budget serves as a roadmap for the country’s economic development and fiscal management.

Objectives of Budget 2026

Budget 2026 has been designed to achieve several key economic objectives, including:

1. Accelerating Economic Growth

The government aims to maintain India’s strong economic momentum by investing heavily in infrastructure, manufacturing, and digital technologies.

2. Promoting Investment

By encouraging domestic and foreign investments, the government aims to strengthen industries and create employment opportunities.

3. Supporting MSMEs and Startups

Small and medium enterprises form the backbone of the Indian economy. Budget 2026 includes measures to improve credit access and reduce compliance burden for businesses.

4. Strengthening Financial Stability

The budget focuses on fiscal discipline, tax compliance, and efficient use of government resources.

5. Expanding Digital Economy

India is becoming one of the largest digital payment economies in the world, and the government aims to further strengthen digital infrastructure.

Major Highlights of Budget 2026

The Union Budget 2026 includes several important announcements aimed at boosting economic development and improving financial stability.

1. Increased Infrastructure Spending

Infrastructure development remains one of the key priorities of the government.

Major infrastructure investments have been announced in:

- Highways and expressways

- Railways modernization

- Urban transport systems

- Logistics parks

- Renewable energy projects

Infrastructure development helps improve connectivity, reduce logistics costs, and stimulate economic growth.

It also generates large-scale employment opportunities, particularly in construction and related industries.

2. Focus on Digital Economy and Fintech

The digital transformation of India continues to accelerate. Budget 2026 emphasizes strengthening digital financial systems and fintech innovation.

Key initiatives include:

- Expansion of digital payment infrastructure

- Strengthening cybersecurity for financial systems

- Encouraging fintech startups

- Promoting UPI-based payment systems

India already processes billions of digital transactions each month, and government support will further strengthen the digital financial ecosystem.

3. Support for MSMEs

Micro, Small and Medium Enterprises (MSMEs) play a crucial role in the Indian economy.

Budget 2026 proposes several measures to support this sector:

- Easier access to business loans

- Simplified compliance procedures

- Credit guarantee support

- Digital lending platforms

These measures are expected to improve liquidity and growth opportunities for small businesses.

4. Manufacturing and “Make in India” Push

Manufacturing is a key driver of employment and exports.

The government continues to promote Make in India initiatives by supporting manufacturing sectors such as:

- electronics

- automobile components

- renewable energy equipment

- defense manufacturing

These initiatives aim to make India a global manufacturing hub.

Tax Changes in Budget 2026

Tax policies announced in the Union Budget directly affect individuals, businesses, and investors.

1. Simplification of Income Tax System

The government continues to move toward a simplified tax system with easier filing procedures.

Key initiatives include:

- Simplified tax return filing process

- Increased digitalization of tax administration

- Faster refund processing

These steps aim to improve tax compliance and reduce administrative burden.

2. Focus on Digital Tax Monitoring

The government is increasing the use of data analytics and technology to track financial transactions and reduce tax evasion.

Integration between different financial systems such as:

- GST

- Income tax

- Banking data

helps authorities improve transparency and reduce tax leakage.

3. Incentives for Long-Term Investments

Budget 2026 encourages individuals to invest in long-term financial instruments.

Some investment areas receiving policy support include:

- mutual funds

- pension schemes

- infrastructure bonds

- retirement savings plans

These measures help individuals build wealth while contributing to economic growth.

Sector-Wise Impact of Budget 2026

Different sectors of the economy are expected to benefit from the policy initiatives announced in Budget 2026.

1. Infrastructure Sector

The infrastructure sector is one of the biggest beneficiaries of the budget.

Increased spending on roads, railways, and urban development will stimulate:

- construction activities

- employment generation

- industrial growth

Companies involved in construction, cement, steel, and logistics may benefit from these initiatives.

2. Banking and Financial Sector

The financial sector is expected to benefit from improved credit availability and financial inclusion initiatives.

Key developments include:

- expansion of digital banking services

- support for fintech innovation

- increased financial access in rural areas

These initiatives aim to strengthen India’s financial ecosystem.

3. Renewable Energy Sector

The government continues to support renewable energy development as part of India’s sustainability goals.

Investments in solar, wind, and green hydrogen projects will help India transition toward a clean energy economy.

4. Technology and Startups

Startups and technology companies are receiving policy support through:

- tax incentives

- funding programs

- innovation initiatives

India has become one of the largest startup ecosystems in the world, and government support will further encourage innovation.

Impact of Budget 2026 on Personal Finance

Budget announcements influence personal finance decisions in several ways.

Understanding these changes helps individuals manage their money more effectively.

1. Tax Planning Opportunities

Changes in taxation rules affect:

- salary structuring

- deductions and exemptions

- investment planning

Individuals should review their tax strategy after the budget to ensure they are using available benefits efficiently.

2. Investment Opportunities

Government spending priorities often influence stock markets and investment trends.

Sectors expected to benefit from Budget 2026 include:

- infrastructure

- renewable energy

- manufacturing

- financial services

Investors may consider diversifying their portfolios to include opportunities in these sectors.

3. Impact on Interest Rates

Fiscal policy and government borrowing influence interest rates in the economy.

Higher government spending may lead to:

- increased borrowing requirements

- potential impact on interest rates

This can affect:

- home loan interest rates

- personal loan costs

- returns on fixed deposits.

Budget 2026 and the Indian Economy

India remains one of the fastest-growing major economies in the world.

Budget 2026 focuses on maintaining this growth momentum by prioritizing:

- infrastructure development

- manufacturing expansion

- digital economy

- innovation and startups

By investing in these areas, the government aims to strengthen India’s position as a major global economic power.

Financial Planning Tips After Budget 2026

Individuals should review their financial plans after every budget announcement.

Here are some practical steps to consider:

Review Your Tax Strategy

Evaluate your current tax planning strategy and explore available deductions and exemptions.

Efficient tax planning helps increase disposable income and long-term savings.

Diversify Your Investment Portfolio

Investing across multiple asset classes helps reduce risk.

Consider diversifying your portfolio with:

- mutual funds

- equities

- gold

- fixed income instruments

Diversification improves long-term financial stability.

Build an Emergency Fund

Financial experts recommend maintaining an emergency fund covering 6 months of expenses.

This fund helps manage unexpected situations such as:

- medical emergencies

- job loss

- sudden financial obligations.

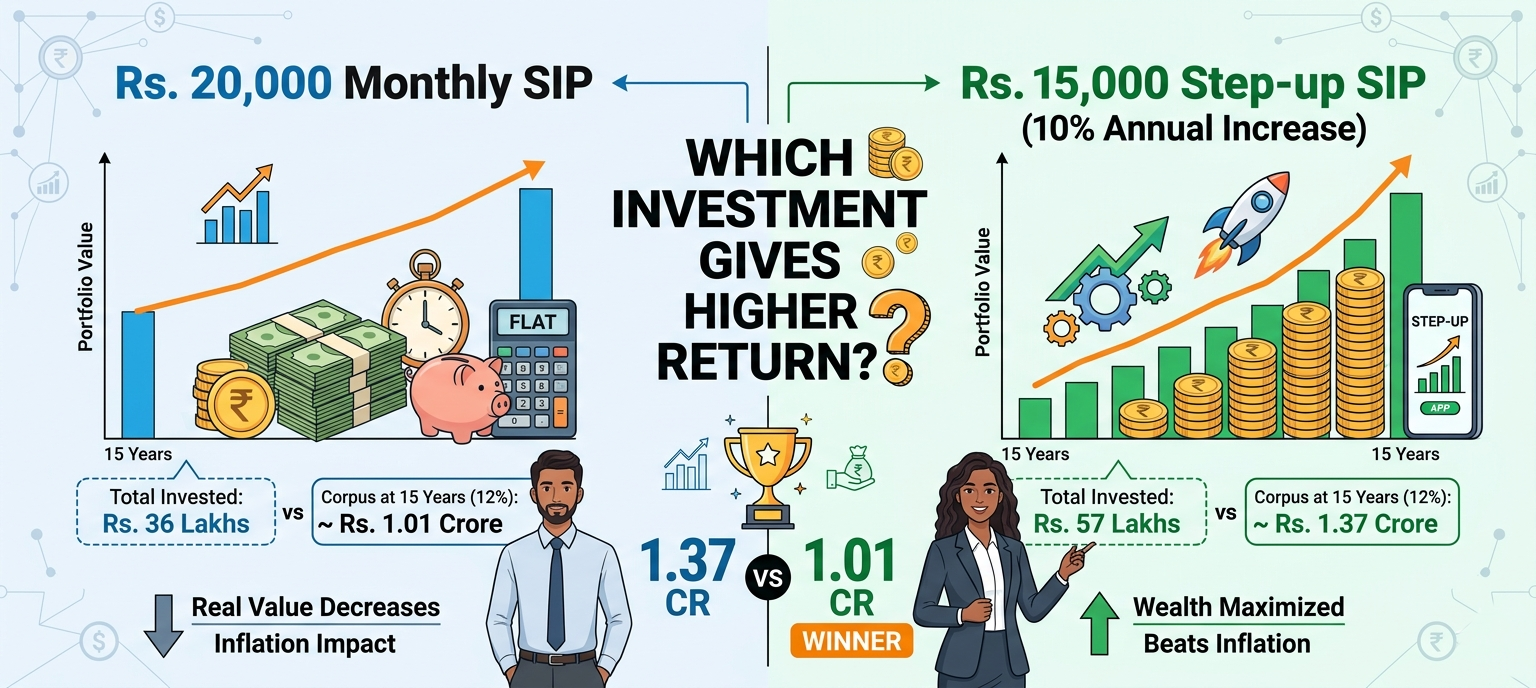

Focus on Long-Term Wealth Creation

Long-term investments such as Systematic Investment Plans (SIPs) and retirement funds can help build wealth over time.

Consistent investing and disciplined financial planning are essential for financial security.

Challenges and Concerns Related to Budget 2026

While Budget 2026 introduces several positive initiatives, some challenges remain.

These include:

- managing fiscal deficit

- controlling inflation

- maintaining sustainable economic growth

Balancing government spending with fiscal discipline will remain an important policy challenge.

Conclusion

The Union Budget 2026 presents a comprehensive strategy to strengthen India’s economy through infrastructure development, digital transformation, manufacturing growth, and financial inclusion.

For individuals and businesses, the budget brings both opportunities and responsibilities. Changes in taxation, investment policies, and government spending priorities will influence financial planning and economic activity in the coming years.

Understanding the implications of the budget allows taxpayers, investors, and entrepreneurs to make informed financial decisions and benefit from emerging opportunities.

As India continues its journey toward becoming a global economic powerhouse, policy initiatives outlined in Budget 2026 will play a crucial role in shaping the country’s financial and economic future.