The debate between a consistent, high-value Systematic Investment Plan (SIP) and a dynamic Step-up SIP is a cornerstone of modern financial planning. For an investor in India, choosing between a flat Rs. 20,000 monthly SIP and a Rs. 15,000 Step-up SIP is not just about the starting amount; it is a battle between immediate capital deployment and the power of incremental growth.

In this article, we will break down the mechanics of both strategies, compare the total outlays, and determine which path yields a higher terminal value over a long-term horizon.

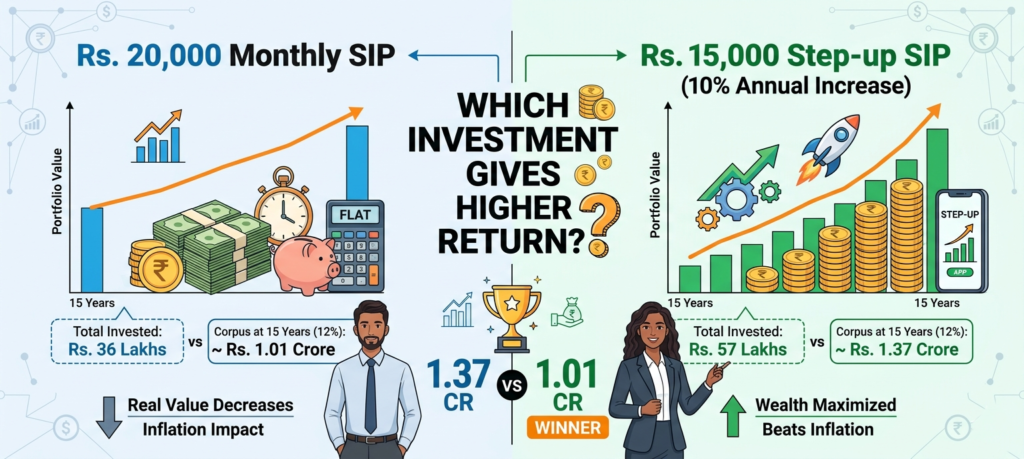

1. Understanding the Contenders

The Flat SIP: Rs. 20,000 Monthly

The flat SIP is the traditional approach. You commit a fixed amount—in this case, Rs. 20,000—every month regardless of market conditions or changes in your income.

-

Pros: High initial “fuel” for compounding. You buy more units early in the investment cycle.

-

Cons: It doesn’t account for annual salary increments or inflation. The real value of Rs. 20,000 decreases over 15–20 years.

The Step-up SIP: Rs. 15,000 Starting + 10% Annual Increase

A Step-up (or Top-up) SIP allows you to increase your contribution by a fixed percentage or amount every year. While it starts lower (Rs. 15,000), it scales with your earning potential.

-

Pros: Disciplined scaling. It forces you to invest your raises rather than succumbing to lifestyle inflation.

-

Cons: A lower starting point means fewer units are accumulated in the crucial first few years.

2. The Mathematical Showdown

To compare these strategies fairly, let’s assume a 15-year investment horizon with an average expected annual return of 12%, which is a standard benchmark for diversified Indian equity mutual funds.

The table below illustrates how the higher initial contribution of the Flat SIP competes against the aggressive growth of the Step-up SIP.

| Comparison Metric | Flat Monthly SIP | 10% Step-up SIP |

| Initial Monthly Investment | Rs. 20,000 | Rs. 15,000 |

| Investment Duration | 15 Years | 15 Years |

| Year 15 Monthly Contribution | Rs. 20,000 | Rs. 56,962 |

| Total Amount Invested | Rs. 36,00,000 | Rs. 57,19,400 |

| Estimated Wealth Gained | Rs. 64,91,520 | Rs. 79,55,905 |

| Total Corpus Value | Rs. 1,00,91,520 | Rs. 1,36,75,305 |

3. Why the Step-up SIP Wins the "Return" Race

At first glance, the Step-up SIP produces a significantly higher corpus—nearly Rs. 36 Lakhs more than the flat SIP. However, it is vital to note that the total amount invested was also much higher in the Step-up scenario (Rs. 57 Lakhs vs. Rs. 36 Lakhs).

The “Compounding Catch-up”

Compounding works best on two variables: Time and Principal.

-

Early Lead: The Rs. 20,000 SIP has the advantage in the first 4 years. Because it puts more money into the market early on, it benefits from more “time” for those specific units to grow.

-

The Overhaul: By Year 5 or 6, the Step-up SIP amount overtakes the flat SIP. From that point forward, the massive increase in principal starts to outweigh the “early start” advantage of the flat SIP.

Even though the Step-up SIP starts with Rs. 5,000 less per month, the 10% annual increase acts like a “turbo-charger.” By the end of the tenure, the sheer volume of capital being injected into the market creates a snowball effect that a flat SIP simply cannot match.

4. Analyzing the "Efficiency" (XIRR)

If we look at the Rate of Return (XIRR), both might show 12%. However, the Step-up SIP is more “Efficient” for a growing career.

Most professionals in India see an annual salary hike of 8% to 12%. If you stick to a flat SIP of Rs. 20,000, you are effectively investing a smaller percentage of your income every year. By choosing the Step-up SIP, you ensure that your investment “share of wallet” stays consistent with your growth.

5. Critical Factors to Consider

Inflation: The Silent Killer

If inflation is at 6%, Rs. 20,000 today will only have the purchasing power of roughly Rs. 8,300 in 15 years. A flat SIP loses its “punch” over time. The Step-up SIP is a natural hedge against inflation because your contributions grow alongside rising costs.

The Psychology of Investing

-

Flat SIP: Easier to manage and automate without thought. It’s “set it and forget it.”

-

Step-up SIP: Requires the discipline to commit more money each year. Many banks and platforms (like AMC websites or Zerodha/Groww) now offer an automated “Step-up” feature, which removes the manual effort.

Risk Tolerance

In the Step-up model, you are investing very large sums (Rs. 50k+) in the final years. If the market crashes in Year 14, the impact on your total corpus is much more severe than in a flat SIP because your “at-risk” capital is higher toward the end.

6. Which is Right for You?

Choose the Rs. 20,000 Flat SIP if:

-

You have a stagnant or fixed income (e.g., rental income or a fixed-increment contract).

-

You are near retirement and want to maximize contributions now while your earning capacity is at its peak.

-

You prefer predictable cash flow and want to use your surplus for other goals like prepaying a home loan.

Choose the Rs. 15,000 Step-up SIP if:

-

You are a young professional or mid-career specialist expecting consistent salary hikes.

-

You want to reach a massive goal (like Rs. 5 Crore for retirement) but can’t afford a high monthly commitment right now.

-

You want to maximize the power of compounding by scaling your principal as your career matures.

Conclusion: The Verdict

While the Rs. 20,000 flat SIP gives you a head start in the first few years, the Rs. 15,000 Step-up SIP is the clear winner for wealth creation.

By starting with a manageable amount and increasing it by just 10% annually, you end up with a corpus that is nearly 35% larger after 15 years. The lesson is simple: It is not just about how much you start with, but how consistently you grow your contribution.

In the world of Indian equity markets, the “Step-up” is the most potent weapon an investor has to turn a modest beginning into a multi-crore fortune. If you have 15 years or more, always choose the Step-up.

Summary Table for Quick Reference:

| Question | Flat Rs. 20k SIP | Rs. 15k Step-up (10%) |

| Winner (15 Years) | Second Place | Grand Winner |

| Ease of Setup | Very High | High (Auto-feature needed) |

| Inflation Hedge | Low | High |

| Best For | Stable/Fixed Income | Growing Professionals |

Frequently Asked Questions (FAQs)

1. Which gives more profit: Starting high or increasing annually?

Investors often wonder if a higher initial investment (like Rs. 20,000) is better than a growing one. The consensus from search trends shows that while a high start accumulates more units early on, a 10% annual Step-up usually creates a significantly larger corpus over 15+ years because the total capital deployed eventually dwarfs the flat SIP.

2. Can I switch my existing regular SIP to a Step-up SIP?

This is a high-volume query for 2026. Most Indian AMC platforms and apps (like Zerodha, Groww, or bank-led portals) now allow you to “Edit SIP” to add a Top-up/Step-up feature. However, many investors search for whether they need to start a new mandate or if the existing bank mandate covers the future increased amounts.

3. What is the “Break-even Point” between these two strategies?

Many analytical investors search for the specific year when a lower Step-up SIP (Rs. 15,000) overtakes the wealth of a higher flat SIP (Rs. 20,000). Mathematically, with a 10% annual increase, the Step-up SIP usually overtakes the flat SIP’s monthly contribution by Year 4 and its total corpus value by Year 7 or 8.

4. How does a market crash affect a Step-up SIP vs. a Flat SIP?

A common concern is “Sequence of Returns Risk.” Investors ask if increasing their SIP during a bull market is risky. The answer often searched is that a Step-up SIP actually helps “Rupee Cost Averaging” better over time, but a crash in the later years of a Step-up SIP hits harder because the monthly investment amount is much larger by then.

5. Is a 10% Step-up enough to beat inflation in India?

With inflation being a recurring theme in 2026, many users ask if a 10% increase is sufficient. Financial experts generally suggest that since India’s long-term inflation hovers around 6%, a 10% Step-up not only covers the rising cost of living but also ensures your “real” savings rate increases as your career progresses.