Old vs New Tax Regime in FY 2026–27: Which One Saves You More?

As we step into Financial Year (FY) 2026–27, the Indian tax landscape has undergone one of its most significant transformations in decades. With the implementation of the Income Tax Act, 2025, and the Income Tax Rules, 2026, the choice between the Old and New Tax Regimes is no longer just a mathematical exercise—it’s a strategic financial decision.

For years, the Old Regime was the go-to for those who loved to save and invest. However, recent budgets have aggressively “sweetened the deal” for the New Tax Regime, raising the tax-free threshold and simplifying slabs. Yet, the 2026 rules have also introduced higher exemption limits for allowances like HRA and children’s education in the Old Regime, creating a tug-of-war for your hard-earned money.

Choosing the wrong regime could cost you thousands of rupees in “lazy tax.” This guide breaks down everything you need to know to pick the winner for your wallet in FY 2026–27.

1. Overview of Both Tax Regimes

The Old Tax Regime: The “Investor’s Favorite”

The Old Tax Regime is built on the philosophy of incentivizing specific financial behaviors. It allows you to reduce your taxable income through a wide array of deductions and exemptions.

- Flexibility: You can lower your tax liability by investing in PF, ELSS, or paying home loan interest.

- Deductions: Includes Section 80C (up to ₹1.5 lakh), 80D (health insurance), and Section 24(b) (home loan interest).

- Exemptions: Includes House Rent Allowance (HRA) and Leave Travel Allowance (LTA).

The New Tax Regime: The “Simplified Path”

Introduced to reduce the compliance burden, the New Tax Regime offers lower tax rates but requires you to forego almost all traditional deductions.

- Simplicity: No need to track investment proofs or insurance receipts.

- Lower Rates: More slabs with lower percentages.

- Default Option: Unless you explicitly choose the Old Regime, you will be taxed under this regime.

Latest Tax Slabs for FY 2026–27

For FY 2026–27, the New Tax Regime has been significantly optimized. The Standard Deduction stands at ₹75,000 for salaried individuals.

| Income Slab (New Regime) | Tax Rate | Income Slab (Old Regime) | Tax Rate |

| Up to ₹4,00,000 | Nil | Up to ₹2,50,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% | ₹2,50,001 – ₹5,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% | ₹5,00,001 – ₹10,00,000 | 20% |

| ₹12,00,001 – ₹16,00,000 | 15% | Above ₹10,00,000 | 30% |

| ₹16,00,001 – ₹20,00,000 | 20% | – | – |

| ₹20,00,001 – ₹24,00,000 | 25% | – | – |

| Above ₹24,00,000 | 30% | – | – |

Note: Under the New Regime, a rebate under Section 87A ensures that individuals with a taxable income up to ₹12 lakh pay ZERO tax.

2. Side-by-Side Comparison Table

| Feature | Old Tax Regime | New Tax Regime (FY 26-27) |

| Tax Rates | Higher (up to 30% after ₹10L) | Lower (30% only after ₹24L) |

| Standard Deduction | ₹50,000 | ₹75,000 |

| Section 80C (LIC, PPF) | Allowed (up to ₹1.5 Lakh) | Not Allowed |

| Section 80D (Mediclaim) | Allowed | Not Allowed |

| HRA & LTA | Allowed | Not Allowed |

| Home Loan Interest | Allowed (up to ₹2 Lakh) | Not Allowed |

| Rebate (Sec 87A) | Up to ₹5 Lakh income | Up to ₹12 Lakh income |

| Best For | High savers & Homeowners | Mid-income earners & Simplifiers |

3. Detailed Tax Calculation Examples

Let’s see how these regimes perform in the real world. (All calculations include 4% Cess).

Scenario A: Salaried Professional with High Deductions

- Gross Income: ₹15,00,000

- Investments: ₹1.5L (80C), ₹50k (80D), ₹2L (Home Loan Interest), ₹1L (HRA).

| Metric | Old Regime | New Regime |

| Total Deductions | ₹5,50,000 | ₹75,000 (Std. Ded) |

| Taxable Income | ₹9,50,000 | ₹14,25,000 |

| Net Tax Payable | ₹1,06,600 | ₹1,02,700 |

| Winner | – | New Regime (Saves ₹3,900) |

Scenario B: Salaried Individual with Minimal Deductions

- Gross Income: ₹10,00,000

- Investments: Only ₹50k in PF (80C).

| Metric | Old Regime | New Regime |

| Total Deductions | ₹1,00,000 | ₹75,000 |

| Taxable Income | ₹9,00,000 | ₹9,25,000 |

| Net Tax Payable | ₹96,200 | ₹0 (Due to Rebate) |

| Winner | – | New Regime (Saves ₹96,200) |

Scenario C: Freelancer / Business Owner

- Net Profit: ₹25,00,000

- Deductions: ₹1.5L (80C).

| Metric | Old Regime | New Regime |

| Total Deductions | ₹1,50,000 | Nil (No Std. Ded for non-salaried) |

| Taxable Income | ₹23,50,000 | ₹25,00,000 |

| Net Tax Payable | ₹5,38,200 | ₹4,47,200 |

| Winner | – | New Regime (Saves ₹91,000) |

4. When Old Regime is Still Better

Despite the push for the New Regime, the Old Regime remains a powerhouse for a specific group of people. You should stick to the Old Regime if:

1. You are Paying a Home Loan: The ₹2 lakh deduction on interest (Section 24b) is a massive shield that the New Regime doesn’t offer.

2. You Live in a Rented House in a Metro: With HRA exemptions now applicable at 50% of basic salary in more cities under the 2026 rules, HRA can significantly tilt the scales.

3. High Section 80D/80C Utilization: If your total deductions (80C + 80D + HRA + Interest) exceed ₹4.25 Lakh for an income of ₹15 Lakh, the Old Regime usually starts winning.

4. Family Benefits: The 2026 rules significantly hiked Children’s Education and Hostel Allowances. If you have two children in hostels, you can now claim nearly ₹2.16 lakh in annual exemptions, making the Old Regime much more attractive.

5. When New Regime is Better

The New Regime is designed to be the “easy button” for Indian taxpayers. It wins when:

1. Income is up to ₹12.75 Lakh: For salaried individuals, the combination of the ₹75,000 Standard Deduction and the ₹12 lakh rebate limit means you pay zero tax without saving a single penny.

2. You Value Liquidity: If you’d rather keep your money in a high-yield savings account or spend it on experiences rather than locking it in a 15-year PPF or 5-year ELSS.

3. Hassle-free Filing: If you don’t want to deal with the stress of collecting rent receipts, insurance certificates, and donation slips.

4. High Earners with Low Deductions: For those earning above ₹25 Lakh, the lower slab rates of the New Regime often outweigh the tax benefits of the Old Regime unless deductions are exceptionally high.

6. Common Mistakes People Make

1. The “Default” Trap: The New Regime is the default. If you don’t inform your HR or select it during filing, you might lose the chance to claim HRA in the Old Regime later.

2. Ignoring the Rebate: Many forget that the ₹12 lakh limit for zero tax only applies to the New Regime. Under the Old Regime, the zero-tax limit effectively stops at ₹5 lakh (taxable).

3. Forgetting “Perks” Tax: New 2026 rules have tripled the taxable value of employer-provided cars. This increases your taxable income regardless of the regime you choose.

4. Switching Without Calculation: Business owners can only switch back to the Old Regime once in a lifetime after opting out. Don’t make the jump without a CA’s advice.

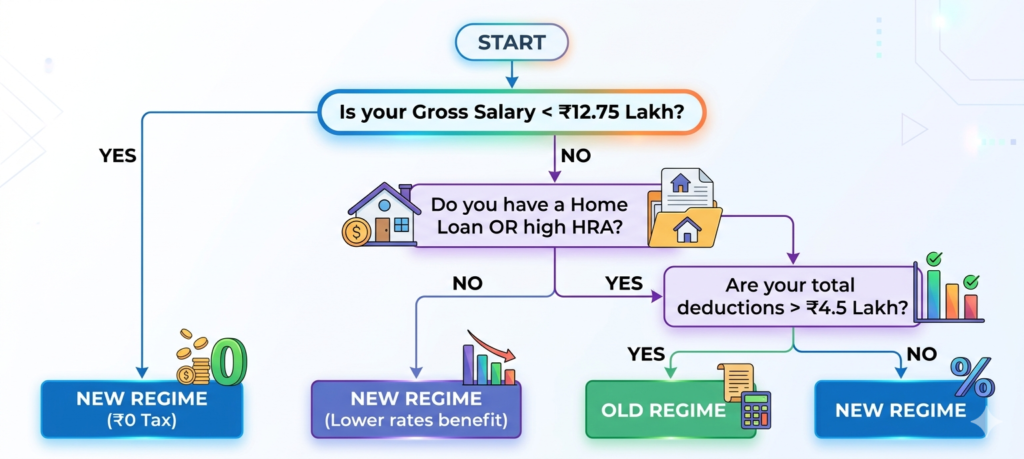

7. Decision Flowchart

8. Pro Tips / Expert Advice

1. The “Rule of Thumb”: If your total deductions and exemptions are less than 30-35% of your gross income, the New Regime is likely your best bet.

2. Annual Review: Your life changes—you might buy a house or get a massive hike. Never assume last year’s choice is right for this year.

3. The Meal Voucher Hack: Under the new 2026 rules, meal vouchers up to ₹1.05 lakh are now exempt in both regimes. Make sure to utilize this regardless of your choice!

4. Invest for Wealth, Not Just Tax: Even if you choose the New Regime, don’t stop investing in your PPF or NPS. Tax should be the result of your financial planning, not the driver of it.

Conclusion

Choosing between the Old and New Tax Regimes in FY 2026–27 is no longer a simple “which is lower” question. With the government pushing for the New Regime through massive rebates for those earning up to ₹12 lakh, it has become the gold standard for the middle class.

However, for the “aggressive savers”—those with home loans, children in education, and heavy insurance commitments—the Old Regime still offers a sanctuary for wealth preservation.

The Golden Rule: Don’t guess. Use a tax calculator or consult a professional. Every taxpayer’s journey is unique, and in the world of taxes, a few minutes of math can save you a month’s salary.

Ignore Keywords: Old vs New Tax Regime FY 2026–27, Which tax regime is better in India, Old vs new tax calculation, Income Tax Act 2025, Section 87A rebate 2026.

FAQs

1. What is the “Tax Year” concept in the Income Tax Act, 2025?

Starting April 2026, the confusing “Assessment Year” (AY) and “Previous Year” (PY) have been merged into a single Tax Year. For example, income earned between April 1, 2026, and March 31, 2027, is simply referred to as Tax Year 2026–27.

2. Do I really pay zero tax if my income is ₹12 Lakh?

Yes, but only in the New Tax Regime. Due to the increased rebate under Section 87A, individuals with a taxable income up to ₹12,00,000 pay no tax. For salaried employees, this limit effectively extends to ₹12.75 Lakh after considering the ₹75,000 Standard Deduction.

3. Is the Old Tax Regime still available in FY 2026–27?

Yes. While the New Tax Regime is the default option, the Old Tax Regime remains available. You can opt for it if your deductions (like HRA, Home Loan Interest, and 80C) significantly lower your taxable income compared to the New Regime’s lower rates.

4. Why has the Securities Transaction Tax (STT) increased?

The government increased STT on Futures (to 0.05%) and Options (to 0.15%) starting April 1, 2026. This was a deliberate move to curb “hyper-speculative” trading in the F&O segment and protect retail investors from high-risk losses.

5. What happened to Form 16 and Form 16A?

They have been replaced. Under the new Act, Form 130 (for salary) and Form 131 (for non-salary TDS) are the new standard certificates. The Income Tax Department introduced these to align with the simplified digital filing process of the 2025 Act.

6. Can I still use Aadhaar as proof of Date of Birth for a PAN card?

No. As of April 2026, the Income Tax Department no longer accepts Aadhaar as valid proof for your Date of Birth on PAN applications. You must now provide a Class X certificate, Passport, or Birth Certificate.

7. I earn ₹6 Lakh but my tax is zero. Do I still need to file an ITR?

Yes. Even if your tax liability is zero due to rebates, you must file an ITR if your total income exceeds the basic exemption limit of ₹4 Lakh (under the New Regime). Filing is mandatory to stay compliant and is often required for loan approvals or visa applications.

8. What is the new rule for buying property from an NRI?

The process has been simplified. From October 1, 2026, resident buyers purchasing property from an NRI no longer need a TAN (Tax Deduction and Collection Account Number). You can now deduct TDS using your PAN and file a simplified “challan-cum-return.”

9. Are Sovereign Gold Bonds (SGBs) still tax-free on maturity?

The rules have changed for secondary market buyers. While original subscribers (who bought directly from the RBI) still enjoy tax-free maturity, those who purchased SGBs from the secondary market (stock exchange) after April 2026 are now subject to Capital Gains Tax.

10. Can I switch between the Old and New Regime every year?

- Salaried Individuals: Yes, you can choose every year at the time of filing your return.

- Business/Professionals: You can only switch once in a lifetime. Once you opt out of the New Regime to go to the Old, you generally cannot move back easily, so choose wisely.